Today I am going to talk about the different types of bond investments. At the end, I will include my three takeaways from this post to hopefully allow you to understand the most important points from this post.

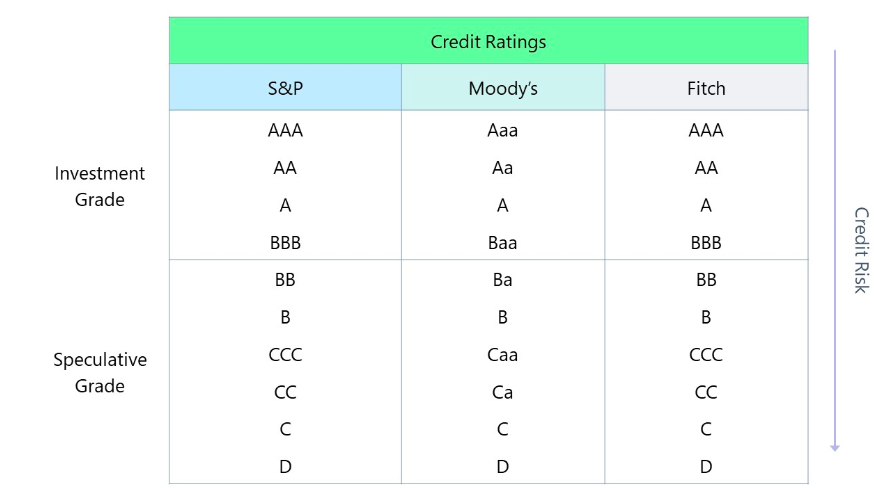

To start, a bond is simply an IOU with simple interest payments(interest only on the investment amount) throughout the period you hold the bond. To begin, I will start by saying that bonds are in general a less risky investment than stocks, but they do not come without risk. For example, if interest rates go up, you may have to sell your bond at a lower price than you paid for it. This is because nobody will pay for a bond with 2% interest when they could get one with 4% interest. Like I said, though, bonds are typically less risky since they are mostly issued by governments. Companies can issue bonds as well to raise money, and their bonds can be very risky and have low credit ratings, or are relatively safe and have high credit ratings. Moody’s, S&P and Fitch rates corporate bonds and they range from a scale shown below.

In regards to actually investing in these bonds, you can go to “Treasury Direct” to buy government bonds. You will need to create an account and link your bank to it in order to get started. You may also go to sites like Vanguard, Fidelity, etc in order to open an account and invest in these products. You may invest in these bonds through a Roth IRA or taxable brokerage account. You can see more info about the Roth IRA in my blog HERE.

Next I want to talk about investing in bonds vs stocks and when to do so. I will say that as you approach retirement you want to have more money allocated in bond investments, and when you are younger/ in your early-mid years in your career, you want to invest mostly in stocks. This strategy is best because stocks have higher growth potential, and if you have a longer time before retirement you can afford and make up for low or negative stock returns. However, if you are approaching retirement, you want to experience less risk and hence, you would want to invest in stocks more then.

Why would I make a whole post dedicated to bonds if my main audience for this is college students and young adults-AKA people who should not invest in bonds now? Well, the first reason is that it never hurts to learn about different types of investments. The second reason is there are a couple accounts and funds that involve bonds or are bond-like in nature that are smart investments for younger people.

Money Market Accounts

Money market accounts are short term bonds of one year or less. Money markets can be useful in times where the Federal Reserve continues to raise interest rates, like they currently are. That way, you can take advantage of the high interest rates in these money market investments. These can be utilized in a couple of ways. The first is, again, by going to Treasury Direct and investing in something called T-bills. This is not the most effective way to invest in money markets, but this is a strategy that can still be effective in times where interest rates are high. The other way is by having your money in a bank such as Ally, Capital One, etc and put your money in a money market account rather than a traditional savings account. Ally currently has a 4% interest rate in their money market account. This is much higher than typical savings accounts that usually return 0.1%-1%. With Ally, they also allow you to get a debit card connected to that account and use it to make purchases 6 times a month. This means your money is much more accessible than it would be in many money market accounts. There are other banks with money market accounts as well such as Fidelity, Citi Bank, Barclays, etc. I would encourage you to research the differences in these accounts to see which fits your situation best before committing to one.

Series I Bonds

Series I bonds are a type of bond investment that can be good in times of high inflation. These bonds seek to have the same interest rate as inflation rate. When inflation is at 5%, the I bonds interest rate is at 5%, for example. In 2022, the interest rate got as high as about 9.5%! This is almost a necessity to invest in for anyone.

Now, this does not come without any downside. You must hold the bond for one year, and if you don’t want to lose out on the last 3 months of interest payments you must hold it for 5 years. This means you can’t access the money until after 5 years. The interest rates also change every 6 months, so you are not guaranteed the same rate for the entirety of the investment. Regardless, it can still be a very useful investment in certain times.

Target Date Funds

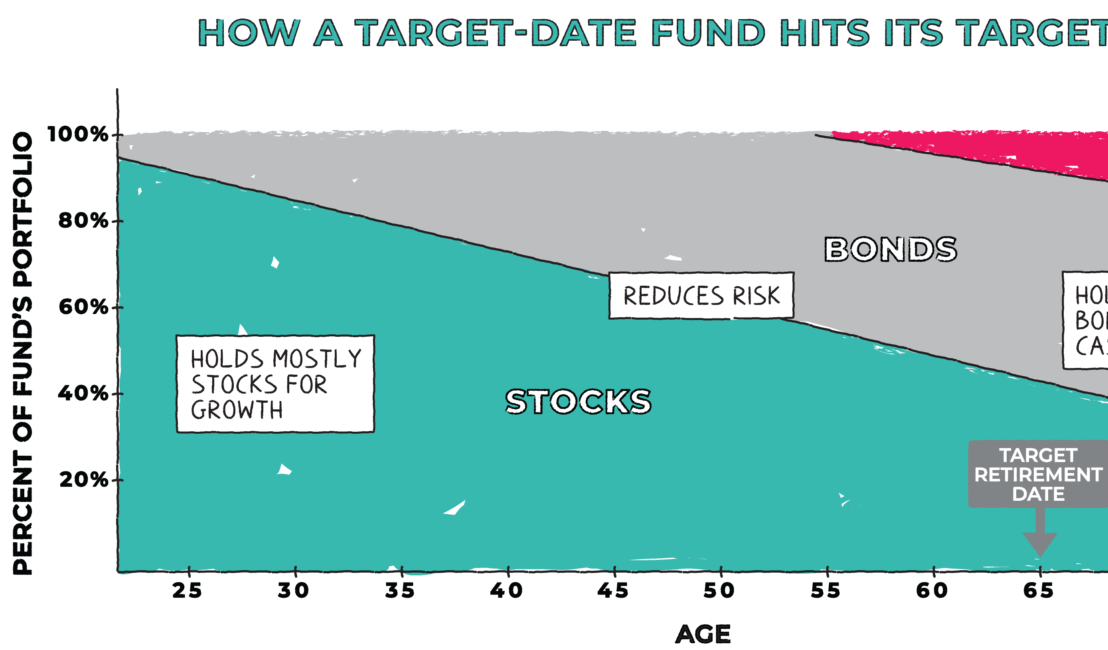

Finally, target date funds are a mix of stocks and bond investments in order to adjust your level of risk throughout your life. For example, if you invested in a target date fund 2065, you would have about 90% in stock investments and 10% in bonds. As the “retirement date” that you picked gets closer, you would see that ratio adjust to have more bond investments than stock investments as you can see below.

These are extremely useful funds for long term, passive investments to get exposure to stocks and bonds. You can invest in these funds through brokers like I have mentioned before such as Fidelity, Vanguard, TD Ameritrade, etc. When you invest in these I would pick a date that represents when you want to retire. If you want even more of the investments in stocks, pick a date that is further out. If you want more investments to be in bonds currently, you can pick a date closer to the current year.

Three Takeaways

1. Don’t prioritize bonds at a young age

2. Utilize money market accounts over typical savings accounts

3. Target date funds are a great way to get bond exposure gradually