Create a plan for yourself

Writing down plans and goals over the next year, 5 years, 10 years, 30 years and when you would like to retire can help you understand a true timeline for your goals. This will allow you to back out and find your savings goals now, and even more so when you get your first full time job(if you are still in college). This will help you also plan out when you start to invest, which types of accounts you want to utilize based on how liquid(easily accessible) you need your savings and investments to be. For example, when you start working a full time job and want to save for a new car you want to buy in 3-5 years you don’t want to put your savings in a 401(k), because you won’t be able to access it until you are 59.5 years old without incurring a 10% penalty.

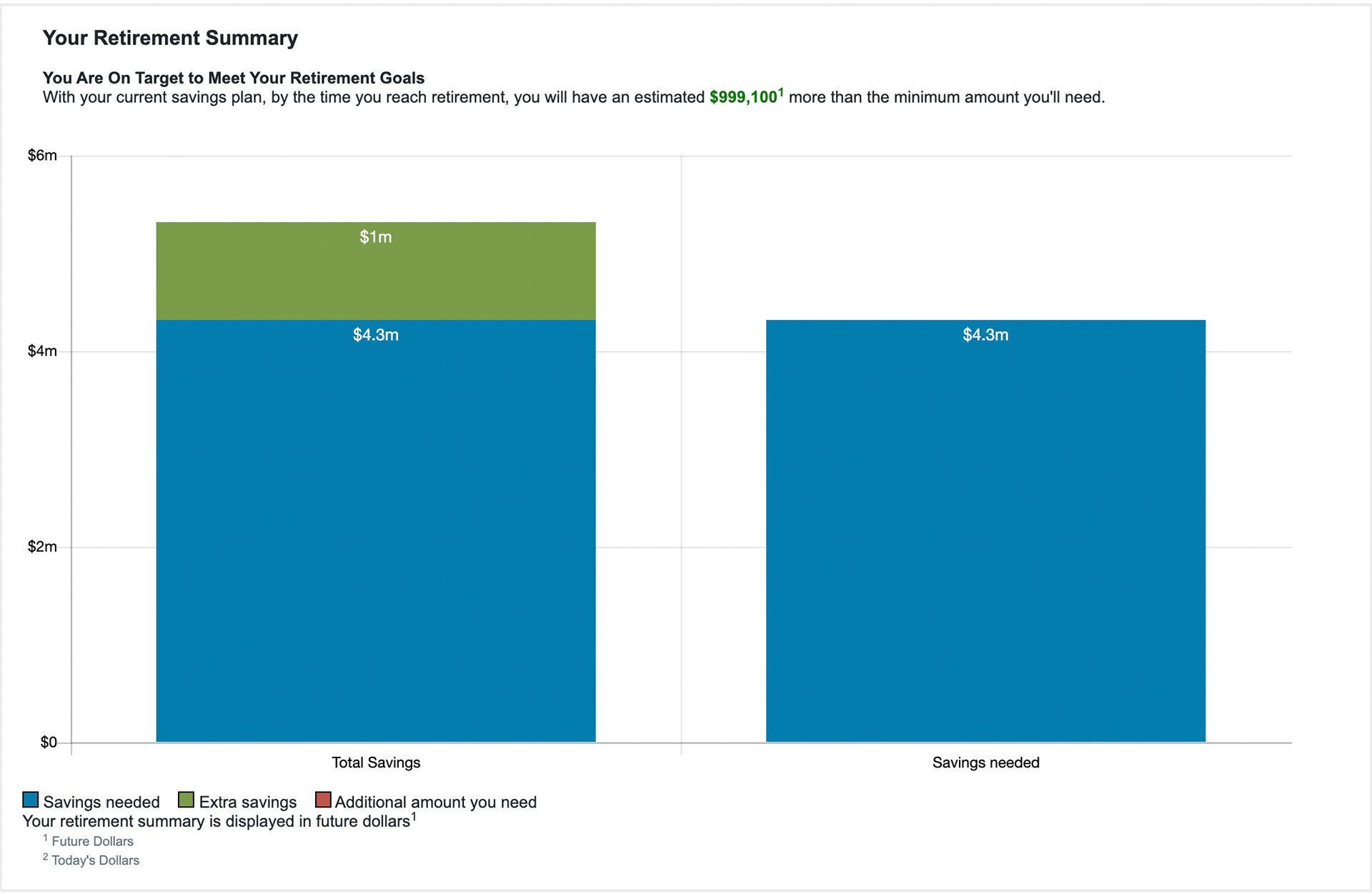

A tool that is incredibly useful for retirement planning is a retirement calculator or financial calculator to figure out how much you will need to save now in order to retire in “X” years. Click the link here to access a great retirement calculator by TD Ameritrade. This calculator will help you determine if you are on track to retire at “X” age with the way you are saving(if working a job currently) or plan to save once out of college. You can also access this retirement calculator in the "resources" tab of this website!

Above is an example of what the results will show you when you fill out the calculator’s questions. If you require more savings, it will suggest adjustments to your savings plan and show you your deficit on the “Savings Needed” bar.

Track your spending

Tracking your expenses can be a useful activity to understand where you need to halt some spending and how you can help reach your savings goals. For me, though, it has helped me behaviorally. When I make myself write down my expenses in a spreadsheet, I think about how much I am spending each week and in turn it will make me internally spend less than I would otherwise. Simply swiping a card and not thinking about it can lead to reckless spending and will also be harder to reach savings goals each week, month, year if you don’t track these things. Setting up a spreadsheet to track these things can be done with relative ease. Click here to see the list of resources I have provided on this site such as a retirement calculator, sites to open investment accounts and a spreadsheet template to track your expenses. Of course there are many ways to track your spending, but the excel/google sheets template gives you a simple and pre-set up option to use.

Open a Roth IRA

A Roth IRA can be opened in less than 10 minutes on any brokerage site like Fidelity, TD Ameritrade, Vanguard, etc. There are many reasons why a Roth IRA is the best account that college students and young adults can utilize now, and I will go through my top 3 reasons as well as give you some suggestions to start investing IN that account.

The first reason this account is so good is that it is an Individual Retirement Account(IRA), which means that all buying and selling of stocks of funds within this account is tax-free! This is huge, because in a typical brokerage account, all trades(buying or selling) in the account result in you having to pay capital gains tax on it.

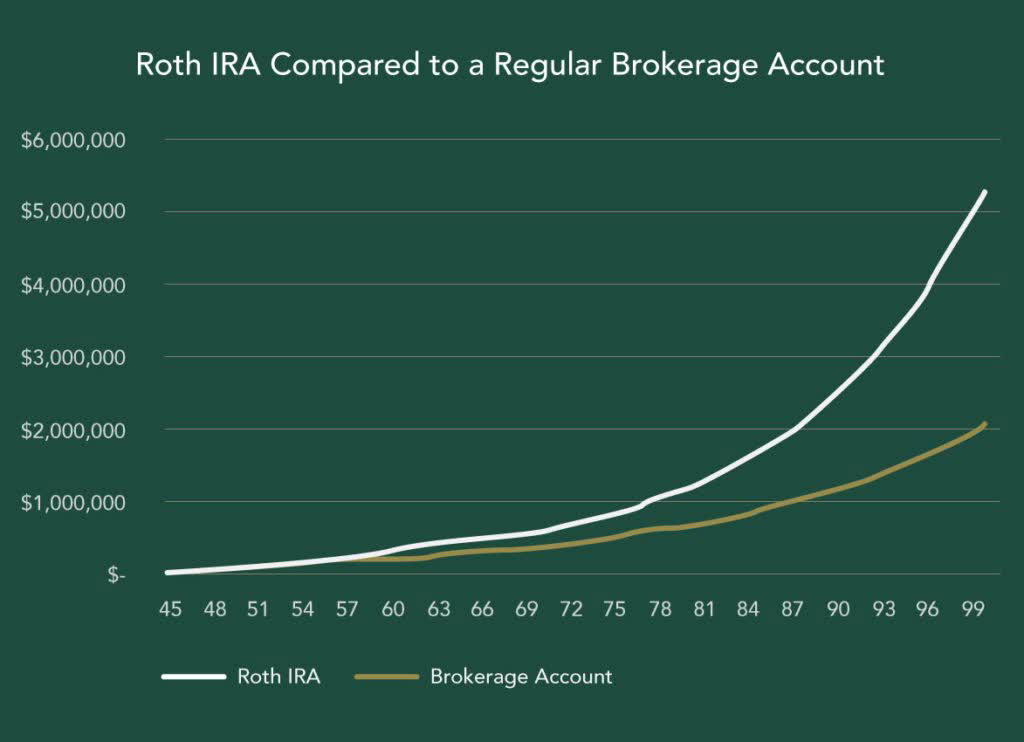

The second reason this account is so good is that when you take out your money from the account when you retire, you have access to them tax-free! This means that at two different points in time where you would get taxed in a typical brokerage account, you avoid taxes altogether. The graph below will show you the effects of using a Roth IRA vs a typical “taxable” brokerage account. The difference is solely due to the difference in taxes paid with each account.

The third reason why this account is so good is that this account can be used as an emergency fund. An emergency fund is something you have probably heard about before, and the Roth IRA can be utilized as such, because any contributions you make to it can be taken out anytime. The interest and gains you make in this account can’t be taken out until you are 59 ½, however.

I have two disclaimers about the Roth IRA. You can only contribute earned income to a Roth IRA. This is because the money you put in has to be after tax dollars. The second disclaimer is that for 2023, there is a $6,500 limit to contributing to a Roth IRA, or up to however much money you have earned in the year(AKA you can't contribute more than how much money you have made that year). However, for 2022 you can still make contributions until tax day(the 2022 limit was $6000).

Now, when it comes to different things you can invest in, I want to talk about index funds and diversification once again. Index funds are an assortment of stocks that aim to bring in the same return as a major stock index such as the total stock market, S&P 500, NASDAQ or Dow Jones. One fund called Vanguard 500 Index Fund ETF(with the ticker VOO) is a great way to immediately become diversified by buying 500 of the largest companies’ stock in one fund. That way you don’t have to buy each stock individually. Buying VOO or a Vanguard Total Stock Market index fund ETF(ticker: VTI) are a simple and passive investment that you can make today in a Roth IRA that will immediately give you diversification in your portfolio. The stock market averages about 10% growth per year, and this is seen historically accurate over the past 100 years. Investing in a diversified fund like VOO or VTI will give you the best exposure to getting those 10% returns by the time you retire.

If you open a Roth IRA today, you will be setting yourself up for success extremely well, while also allowing yourself the access to your contributions if they are ever needed!

Sources

https://seekingalpha.com/article/4443933-building-tax-free-portfolio-8-percent-yields-double-digit-total-returns