Today I will be talking about the good and the bad about credit cards, and how different people should approach the decision to get one or not. I will start out by saying that getting a credit card is a decision each person has to make themselves, and the people who should get one are typically those who are self disciplined and know themselves very well. Credit cards in and of themselves are not bad, in fact they can be extremely useful, if used correctly and effectively.

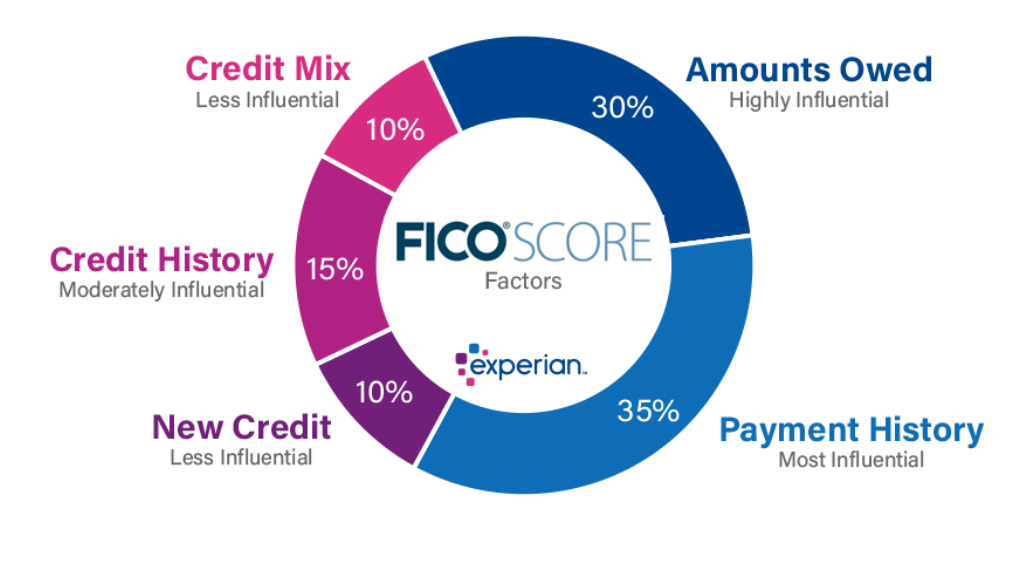

To start, I will discuss credit scores and what goes into a credit score. Credit scores are used if you need a loan for a house or car primarily. First off, as long as you have some form of credit(i.e. Have a credit card), you will start to build a credit score. Over time, as you build a credit history of reliably paying on time, you will increase your score. Secondly, your credit score will take a hit if you eat into a large amount of your credit limit. If you have a monthly credit limit of $5,000, and you spend, say, $4,500 for a long time, your credit score could take a small hit. Finally, getting a “hard inquiry” on your credit score to apply for a loan may affect your credit score. For example if you get five different banks to pull your credit score for the sole reason of potentially getting a loan you will most likely experience a temporary drop in your credit score. For contrast, if a company does a “soft inquiry”, to check your score as a part of a background check or without you knowing, your score will not be affected. You can see a graph below with how much each factor plays into credit scores.

Cash Back Perks

The first type of perks that you can take advantage of with Credit Cards is cash back. How this works is every month the credit card company will issue you your statement, and for certain purchases you will get a percentage of the amount paid on those purchases back in cash. For example, if you have a card that offers you cash back on gas and grocery store purchases, if you spend $1,000 on gas and groceries that month and you have 2% cash back, you will get $20 back in cash that month. It may not seem like a lot, but if you consider utilizing this perk over 10,15, even 20 years the rewards are well worth it. You can look at this perk as allowing you to spend, in this case, 2% less on every gas and grocery purchase.

In case you are also curious about Roth IRA’s, you can get a Fidelity credit card, and if you have a Fidelity Roth IRA, you can deposit any cash back earned into that account. This allows the cash back to grow as well! If you need more information on a Roth IRA, click HERE. You can see the Fidelity credit card site at the link below the image.

Point Perks

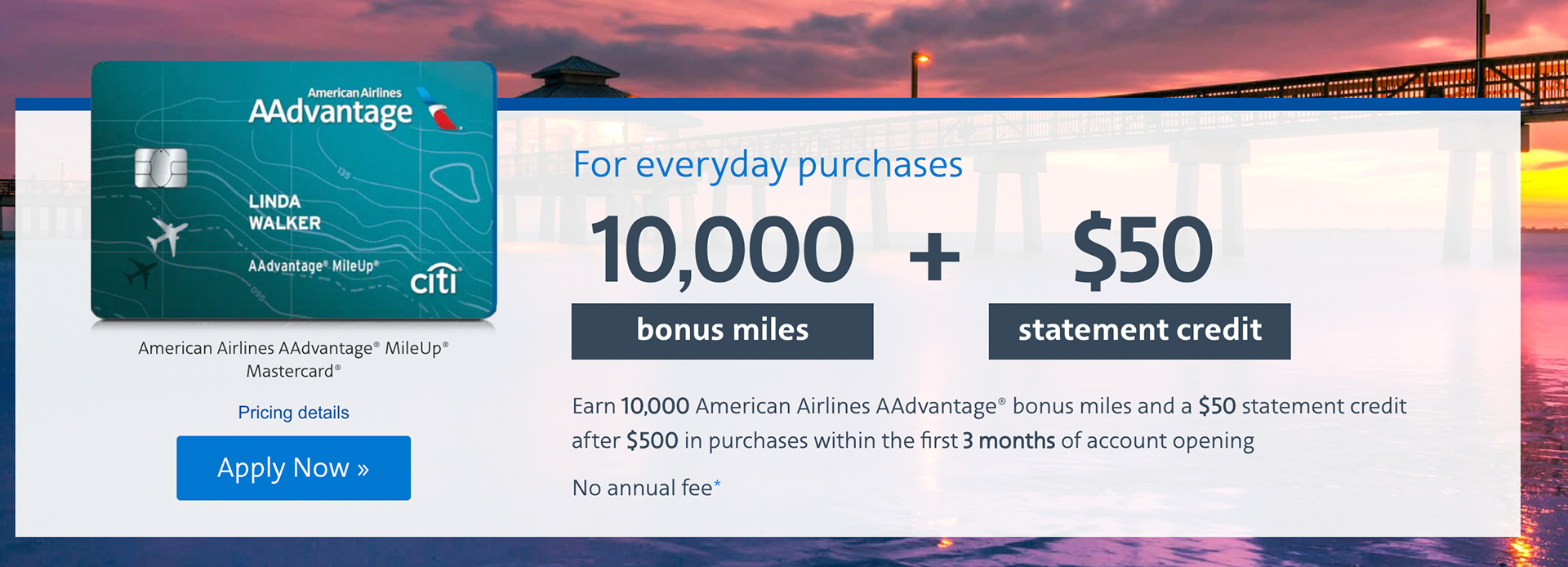

Point perks are the second, and sometimes more lucrative perk of credit cards. Many point perks will work by setting a certain amount of money you must spend in the first certain number of months of having the card in order to get the point perks. For example, the graphic below shows American Airlines’ base credit card perks.

Of course, these perks don’t come solely with points with a company. For example, Southwest has a credit card that allows you to get a companion pass with Southwest(a guest flies for free). These perks can be very valuable, and SHOULD be utilized. As long as you pay off your credit card bill on time, these are good perks. Of course, you should not spend more than your means simply to get these perks.

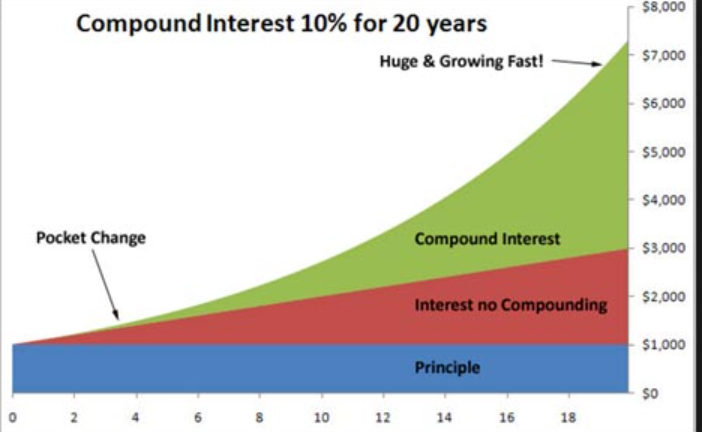

Finally, credit cards do have two main downsides. To begin, I don’t want you to be disheartened and think credit cards are only bad, because they do have great factors, but if you aren’t careful credit cards can cripple your financial future. The first and much more manageable downside is that many non-base credit cards have an annual fee. Usually it ranges from around $95 to $300. This isn’t bad, however you should be aware of this going into getting a credit card. Secondly, credit cards have LARGE interest rates that compound. Usually this ranges from 20% to 35% depending on your credit score. This is why it is so important to pay off your credit card bill on time. Once you start accruing interest on your payments it is nearly impossible to pay off. If you just have $500 you haven’t paid off, that will gain 20%-35% interest annually, and compound which means the interest builds on itself, it is not just calculated on the $500. You can see below how fast these interest payments can grow when they compound.

This is why you must know yourself before getting a credit card, and why you shouldn’t spend above your means on a credit card!

Takeaways:

1. Know yourself when getting a credit card, they can be a good financial tool!

2. Cash back and point perks should be taken advantage of